strategy

Research

Project Juniper

A scalable, HOA-led system for community wildfire mitigation in WUI communities

TL;DR

Work Type

Team of 4

Timeline

Sep 2025 - Dec 2025 (4 months)

Context

Client project in class

Tools Used

Business Model Canvas, Empathy interview

Project Goal

Help our client translate years of wildfire research into a scalable, HOA-led system that enables community-level mitigation in WUI zones.

key Challenge

Balancing the client’s ambition for a comprehensive, system-wide solution with limited team capacity and a fragmented partner ecosystem.

key Approaches

Business Planning, Dual-path GTM Strategy, Ecosystem-Led Collaboration

Context

Defining the WUI Wildfire Challenge

Our clients have spent years studying wildfire mitigation in Wildland–Urban Interface (WUI) communities. Through their research, one conclusion became increasingly clear:

The science is no longer the problem.

Evidence now clearly shows which interventions—particularly zone zero mitigation, home hardening, and defensible space—significantly reduce structure loss.

Behavioral resistance—not knowledge gaps—is the real barrier.

Although the pathway is clear, people still refuse to act on what works. Cultural norms, cost perceptions, coordination challenges, and lack of shared accountability prevent widespread adoption.

Design Principles

To address wildfire risk at the community scale, we grounded our solution exploration in the following principles:

1. Design for Community, Not Individuals

Mitigation must function at the neighborhood and zone level, recognizing interdependence between properties and shifting responsibility from lone homeowners to shared systems.

2. Normalize the Right Behavior

Zone zero mitigation should feel standard, visible, and socially reinforced—not exceptional, alarmist, or optional. Cultural norms are as critical as technical compliance.

3. Reduce Friction to Act

Solutions must minimize cognitive, financial, and logistical barriers by orchestrating services, timelines, and decisions rather than asking homeowners to self-coordinate.

4. Align Incentives Across Stakeholders

Homeowners, HOAs, insurers, service providers, and municipalities must all benefit from participation, creating positive feedback loops that reward prevention over recovery.

5. Build for Long-Term Momentum

Wildfire mitigation cannot be a one-off campaign. The system must sustain engagement over time, enabling continuous upkeep, accountability, and community ownership.

Customer

Choosing the Right Customer to Activate Change

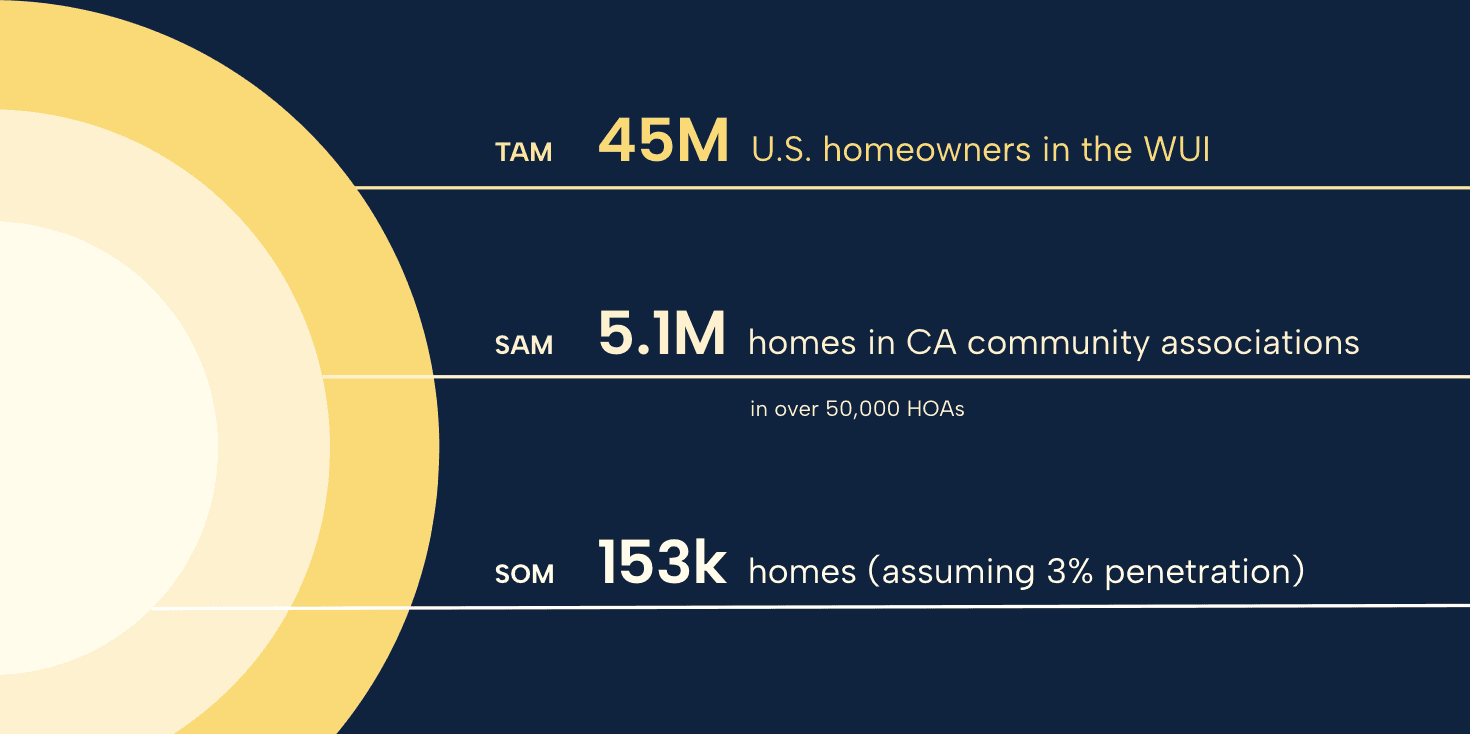

Gauging the market size

We began by understanding the scale of the problem through a TAM / SAM / SOM analysis, estimating how many households are affected by wildfire risk in WUI zones.

Finding the right customer

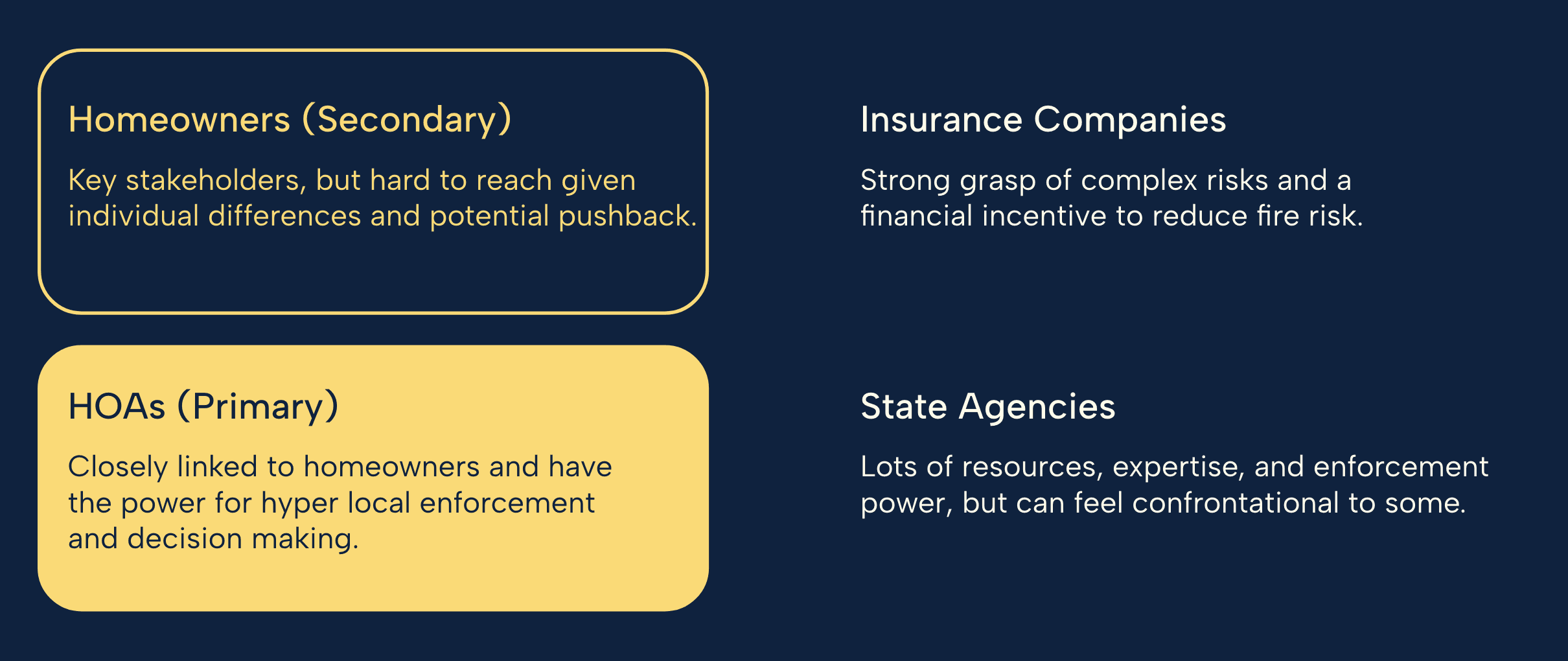

We did a stakeholder analysis for all parties in the ecosystem, and divide them based on power and interest.

From there, we examined four primary stakeholder groups involved in wildfire mitigation.

Through this analysis, HOAs emerged as the most leveraged entry point.

Rather than asking individual homeowners to act alone, we chose to design around HOAs as the primary customer—using them as the organizing unit to unlock community-level wildfire resilience in WUI zones.

The challenge, then, is not simply motivating individual homeowners—but enabling HOAs to orchestrate collective action across diverse residents, service providers, and constraints.

Our Vision

We seek to enable HOAs to systematically reduce wildfire risk by aligning homeowners, services, and incentives into a scalable, self-sustaining model.

Research & insights

Voices from the communities: Barriers to Collective Action

5+2 Interviews

To understand what this would require in practice, we conducted in-depth interviews with HOA leaders and wildfire experts to uncover the real barriers preventing action on the ground.

Key Insights

HOAs can initiate action—but with limitations.

Even in planned communities with HOAs, collective action is hard to encourage. Education, social norms, and financial incentives are critical to overcoming inertia and sustaining collective action.

One-size-fits-all guidance doesn’t work.

Each WUI community faces unique environmental, structural, and regulatory conditions, requiring tailored expert guidance and locally appropriate service coordination.

Home value is a more powerful motivator.

Tying wildfire mitigation to property value and long-term asset protection resonates even with homeowners who are otherwise disengaged from fire risk.

Affordability is the final determinator.

Upfront costs remain the primary bottleneck. Without accessible financing, incentives, or cost-sharing mechanisms, even motivated communities struggle to act.

These aligned with our previous hypothesis and also paved our way to the business structure.

“You can put tens of thousands of dollars into making your home fire safe... but if your neighbors don’t, it doesn’t mean anything.”

-Jim, HOA Board Member, Winter Creek, Tahoe

ideation

scope up & narrow down

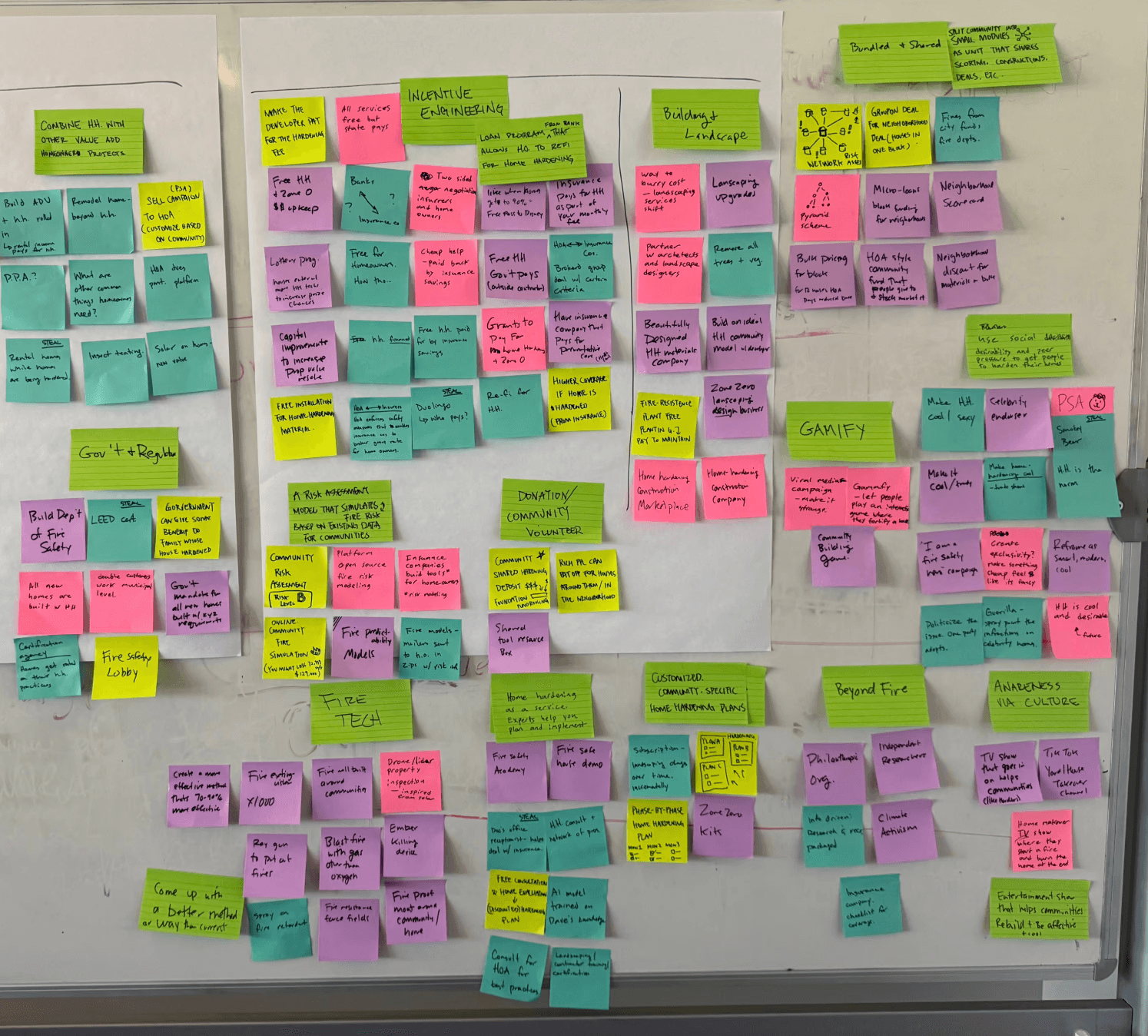

Business Model Brainstorming

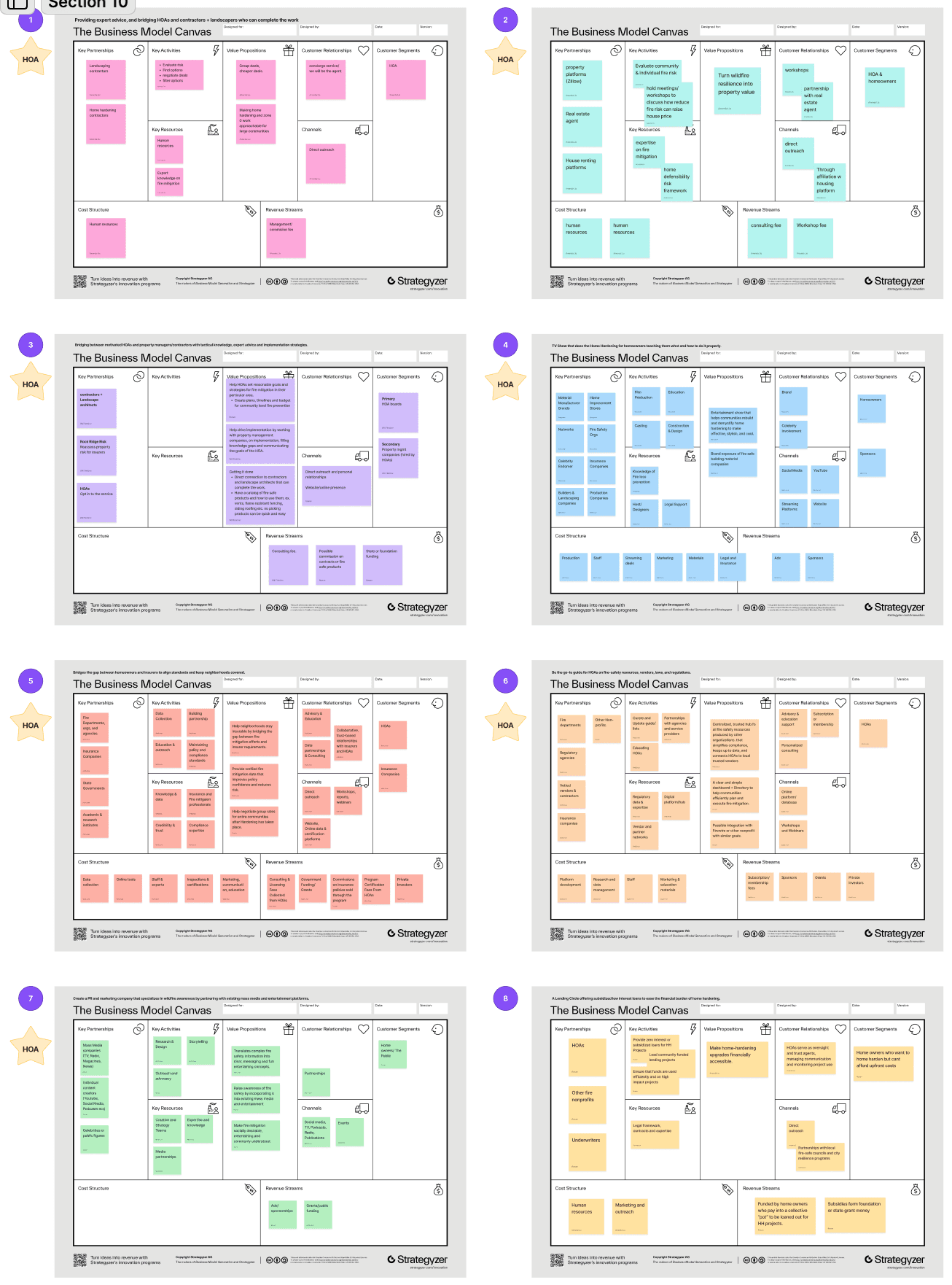

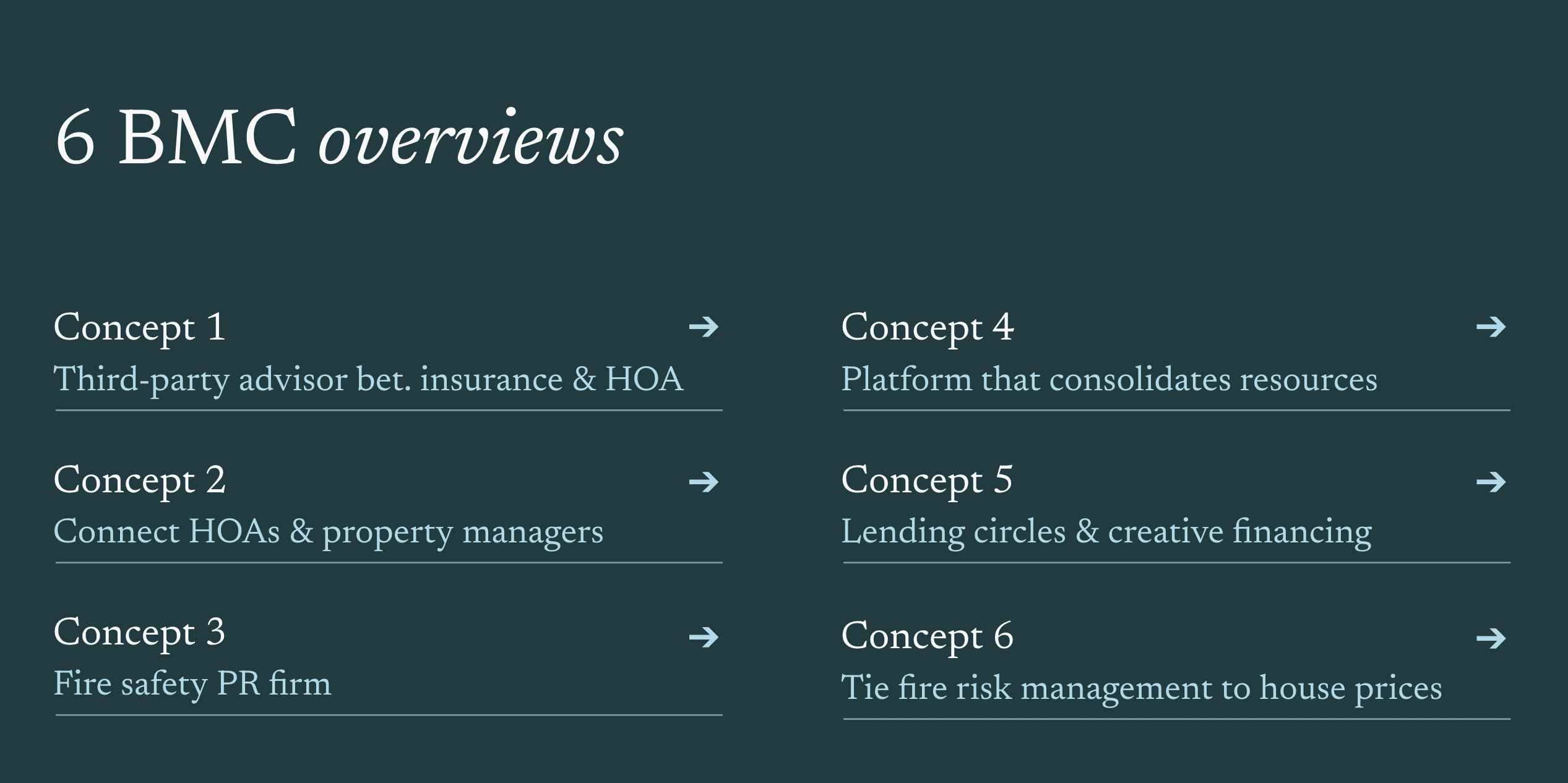

We began by brainstorming ideas, each target one insight/pain point from the interview. Then we turned some of the strongest ideas into Business Model using the Business Model Canvas.

Concept Evaluation & Down-Selection

We presented 6 of our strongest business model to the clients.

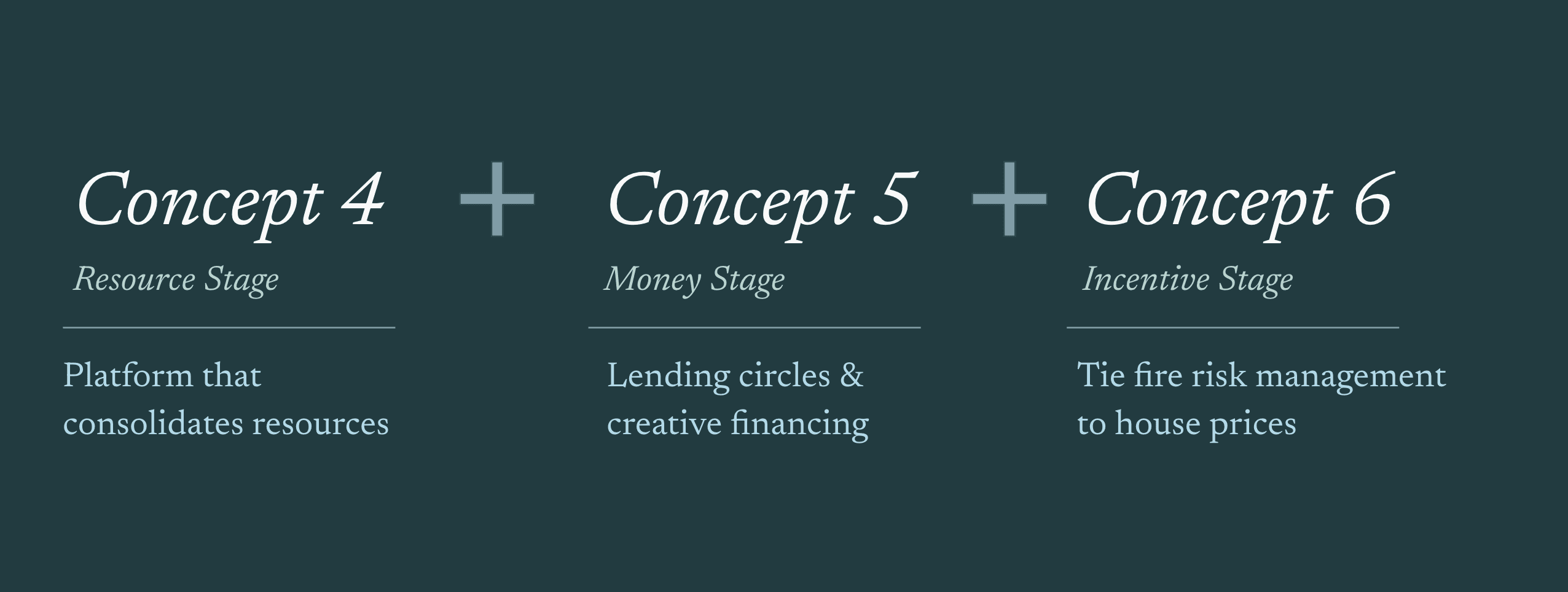

We evaluated each concept against our core insights—HOA leverage, affordability, and behavior change—and found that no single model could solve the problem alone.

The strongest path forward was a stacked model that addresses resources, financing, and incentives as one system.

Together, these form a single, integrated system: access to clear guidance enables action, financing removes cost barriers, and incentives sustain long-term participation.

Concept Testing + Validation

Integrating the system: Where Willingness Meets Friction

To evaluate whether the proposed system could function as a viable business, we tested it along two complementary methods:

Method 1: Quantitative validation test with homeowners.

Method 2: Qualitative viability test with HOAs

Together, these tests allowed us to assess both organizational adoption (HOAs as the primary customer) and end-user willingness to pay (homeowners as the final customer).

Method 1: Quantitative Validation — Homeowner Willingness Test

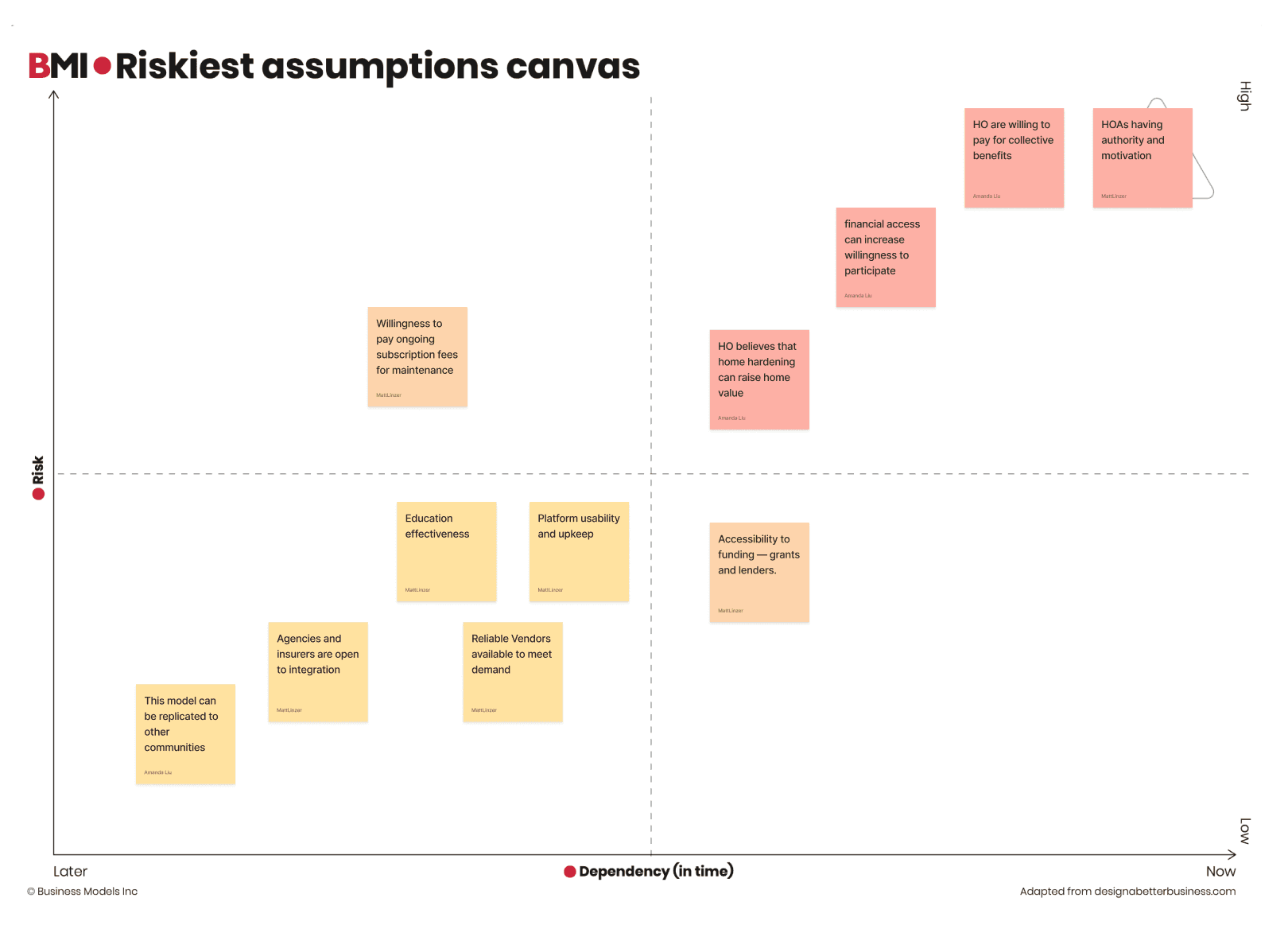

Because homeowners are the final-stage customer and primary payer, we designed a survey to validate core behavioral and economic assumptions.

The survey was structured around key hypotheses derived from a Risk Assumption Canvas, including—but not limited to:

Homeowners are willing to pay for collective, community-level benefits

Homeowners are open to HOA-initiated wildfire programs

Home value, insurance access, and community safety increase willingness to participate

This quantitative path allowed us to test scale, directionality, and sensitivity—verifying whether the model could realistically convert HOA action into homeowner participation.

This quantitative path allowed us to test scale, directionality, and sensitivity—verifying whether the model could realistically convert HOA action into homeowner participation.

We sent the survey out to several WUI communities and received 17 responses. Here are what was validated:

What the Data Confirmed

50% of the participants chose cost as the primary blocking factor to home hardening.

>> Financial accessibility must be a core pillar of the business model—not an add-on.

82% believe wildfire risk should be addressed at the community level, not by individual homeowners alone.

>> Positioning the program as a community project (vs. individual upgrade) increases legitimacy and buy-in.

100% reported higher motivation if others in their community were also taking action.

>> Participation increases when neighbors act together.

87% expressed interest in paying an additional >$20/month through HOA dues for community home hardening.

>> Homeowners are willing to adopt a shared-risk, shared-investment financial model.

66.7% believe wildfire-resistant upgrades increase property value

>> Validates property value as a credible motivation lever—but not a universal one.

Method 2: Qualitative Validation — HOA Viability Test

We designed a “fake door” test to evaluate whether HOAs would opt into the program in principle—and what conditions would shape their decision.

Using a concept brochure that described the program’s structure, services, and value proposition, we conducted interviews with HOA members to simulate a real decision-making moment.

This test helped us understand:

Whether HOAs would see wildfire mitigation as within their mandate

What objections, concerns, or decision criteria emerged

What would need to be true for participation to feel feasible

Rather than testing features, this pathway tested organizational buy-in—a critical prerequisite for any HOA-led model.

From our user test with HOA members, we uncovered the following insights:

What Was Validated

Community-specific tailoring is not optional—it’s foundational.

Each HOA operates within unique environmental, regulatory, and social conditions, confirming that expert-led, customized guidance is essential at every stage of mitigation.

Mitigation must be treated as a long-term system, not a one-time intervention.

Stakeholders emphasized the need for ongoing monitoring, phased implementation, and progressive planning to sustain impact over time.Linking mitigation to home value resonates more than risk alone.

For disengaged homeowners, ROI framing—particularly property value protection—proved far more motivating than abstract wildfire risk.

What Introduced Friction or Risk

Creative financing shows promise but faces regulatory uncertainty.

While alternative financing models lowered psychological barriers to action, they may require careful structuring to navigate legal and insurance constraints.

Execution is labor-intensive—even with HOA buy-in.

Coordinating assessments, services, and homeowner participation demands significant effort, reinforcing the need for operational focus and clear scoping.

What This Changed in the Model

Targeted community selection became critical.

Rather than pursuing broad adoption, the model must start with high-risk communities where wildfire threat is acute and leadership is motivated.

Leadership readiness became a gating criterion.

Successful implementation depends on working with HOAs that have a clear champion capable of sustaining momentum.Expert orchestration emerged as a core value proposition.

Beyond tools or financing, the primary value lies in guiding communities through complexity—end to end.

As a Conclusion:

Testing revealed that while the model is viable, its success depends on deep tailoring, long-term engagement, and disciplined community selection rather than broad, one-size-fits-all deployment.

Partnership

Market Signal: An Existing System in Motion

Throughout interviews with HOA leaders and fire experts, a recurring reference emerged: Fire Smart Community Pilot by the Tahoe Fund, which already operating in this space.

Fire Smart is actively addressing community wildfire mitigation by coordinating assessments, education, and mitigation efforts across WUI communities. Unlike many fragmented initiatives, they have already launched, gained traction, and demonstrated early momentum.

Rather than invalidating our concept, Fire Smart served as a strong market signal:

The problem is real and urgent

Stakeholders are willing to engage

System-level approaches can move from theory to practice

What We Learned from the Pioneer

We interviewed Tahoe Fund's Chief Program Officer and gained some insights:

Scaling requires coordination, not ownership.

No single organization can deliver end-to-end wildfire mitigation alone. Effective implementation depends on a constellation of partners—experts, service providers, financiers, HOAs, and public agencies—working in concert.

The ecosystem is actively seeking integrators.

Organizations in this space are looking for partners who can simplify, coordinate, and operationalize community adoption, rather than introduce yet another standalone program.

These ecosystem signals shaped our go-to-market strategy, framing a clear choice between joining an existing system-level effort or entering the market by owning a focused, high-leverage role within it.

GTM Strategy

From Validation to Go-to-Market

With validated demand but constrained capacity, our go-to-market strategy explored two paths: orchestrating the full ecosystem—or entering through a focused, high-impact niche within it.

Why two paths?

Pathway A reflects the client’s long-term vision for a system-level solution, amplified through collaboration with Fire Smart.

Pathway B reflects near-term execution reality, enabling focused entry within existing capacity constraints.

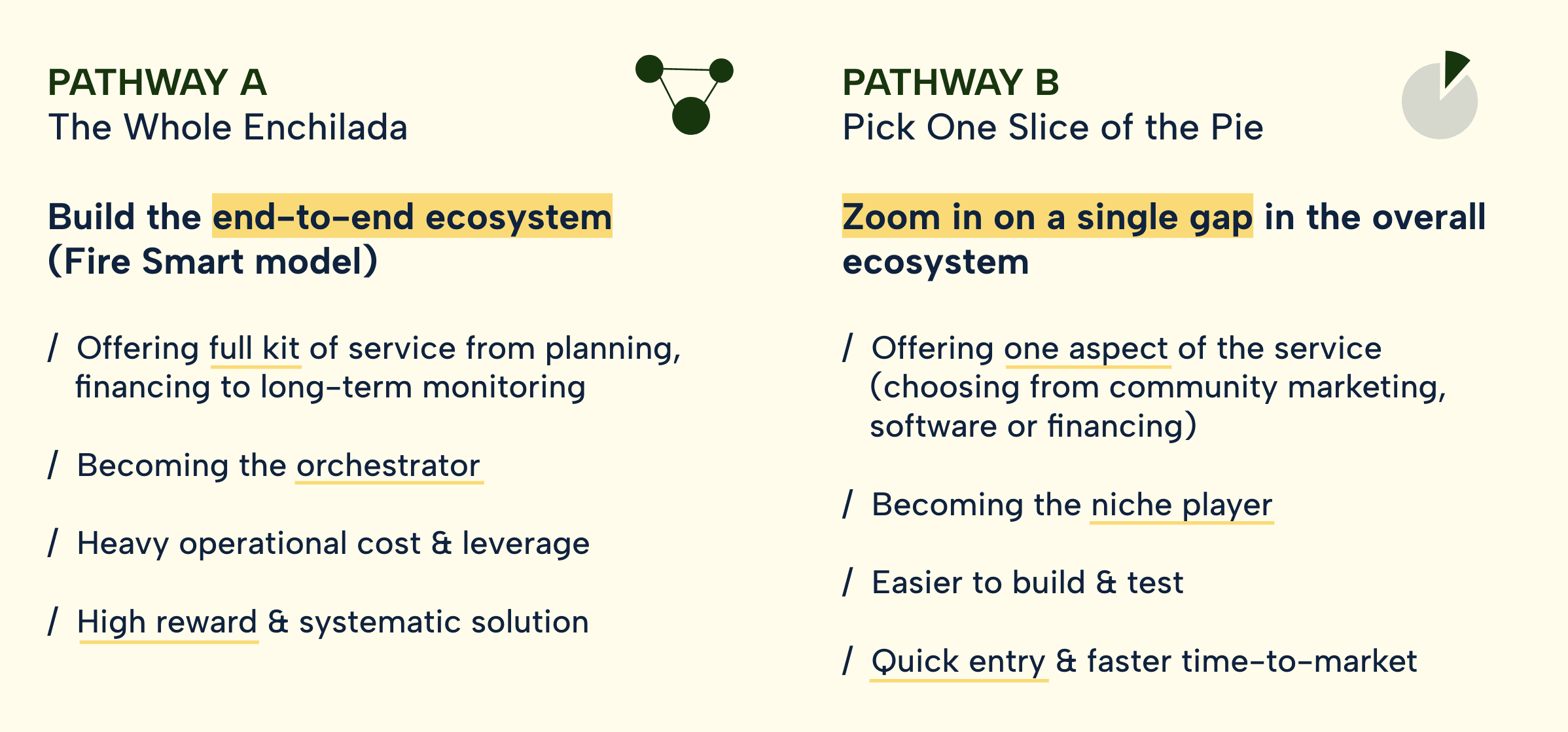

Pathway A: System Path

Pathway A leans into system orchestration, building or joining a full end-to-end ecosystem capable of coordinating planning, financing, execution, and long-term monitoring.

Rather than duplicating existing efforts, Pathway A positions Juniper as the coordinating layer that works alongside organizations like Fire Smart (Tahoe Fund) to translate proven models into scalable, repeatable community systems.

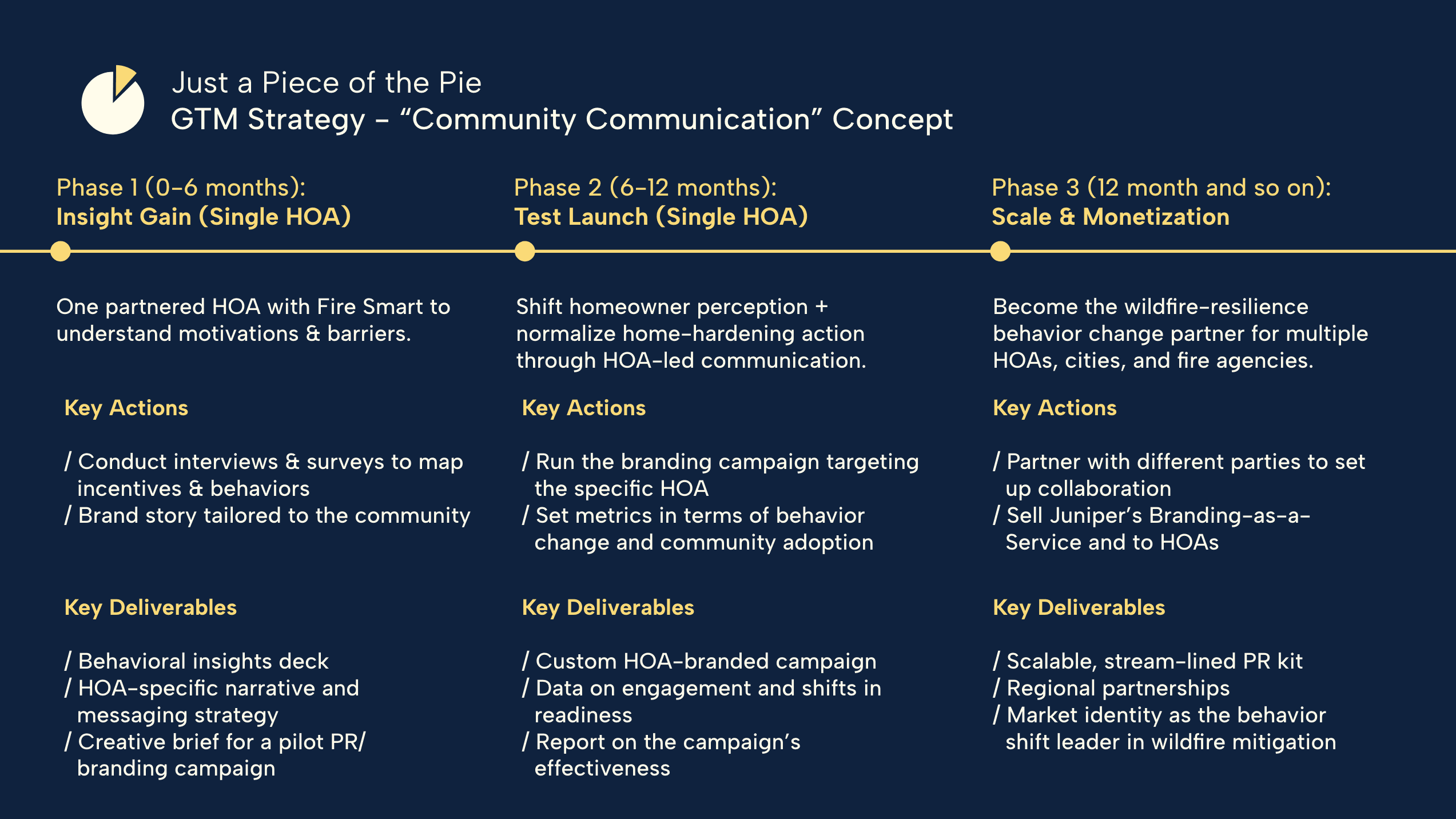

Pathway B: Niche Path

Rather than replicating a full end-to-end system, Pathway B explores focused entry points where Juniper could complement and strengthen existing models like Fire Smart—by owning the pieces that are hardest to scale or least well supported today.